Affiliate Disclosure: This article contains affiliate links. If you click and purchase through them, I may earn a small commission at no extra cost to you. I only recommend tools I genuinely believe are worth your time.

Let’s be real. Most budgeting advice assumes you already have your act together. But what if you genuinely struggle with money – overspending, forgetting bills, living paycheck to paycheck? That’s exactly who this article is for.

The good news is that the right app can make a real difference. People who use budgeting apps consistently save an average of 20% more money per year than those who don’t. The trick is finding one that works for how your brain actually works, not how a finance textbook thinks it should.

Here are the best options for 2026, broken down honestly.

1. YNAB (You Need a Budget) – Best Overall for Breaking Bad Money Habits

If you’re genuinely bad with money, YNAB is the app most likely to actually change that. It’s not just a tracker – it’s a method.

The idea is simple: every dollar you earn gets assigned a job before you spend it. Rent, groceries, subscriptions, fun money – each gets its own category. When you run out in one category, you move money from another. This forces you to make conscious decisions instead of spending on autopilot.

It costs around $14.99 a month (or $99 a year), but it comes with a 34-day free trial. People on YNAB report saving an average of $600 in their first two months, which more than covers the cost.

Best for: People who want real structure and are ready to actually engage with their money.

2. PocketGuard – Best for Chronic Overspenders

PocketGuard answers one question: how much can I actually spend right now without messing up my finances?

It connects to your bank, looks at your bills, savings goals, and upcoming expenses, then tells you exactly what’s safe to spend today. No spreadsheets. No categories to set up manually. Just a clear number.

A newer feature called “Pace” even alerts you if you’re burning through your monthly budget too quickly based on how many days are left. It’s the kind of guardrail that overspenders actually need.

There’s a free version, and a PocketGuard Plus upgrade for more detailed features.

Best for: People who need simple, no-brainer guardrails on their daily spending.

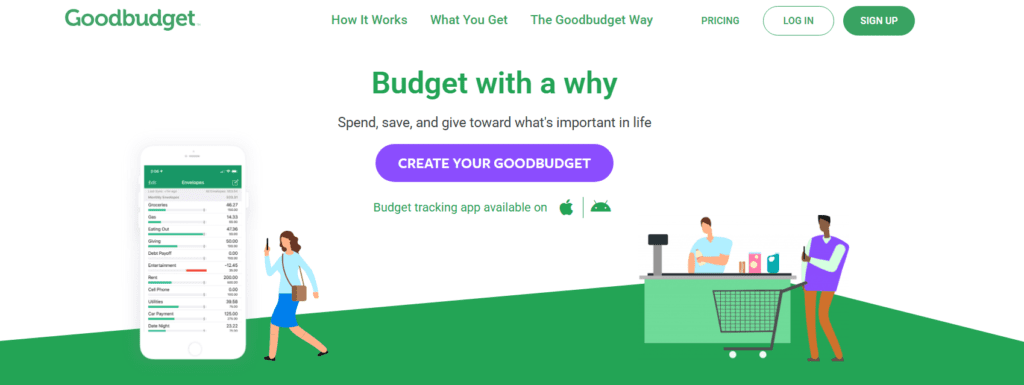

3. Goodbudget – Best Free App for Beginners

If you’ve ever heard of the “cash envelope” method – where you put physical cash in envelopes for different spending categories – Goodbudget is the digital version of that.

You don’t connect your bank account in the free version. You manually enter what you earn and what you spend. That sounds tedious, but for people who are bad with money, the act of manually tracking creates awareness that automatic syncing doesn’t.

The free tier gives you 10 spending envelopes and a year of history. It also works well for couples since you can share the budget across two devices.

Best for: Total beginners or anyone who wants free, simple envelope-style budgeting.

4. EveryDollar – Best for People With Debt

Built by Dave Ramsey’s company, EveryDollar follows the zero-based budgeting approach – meaning every dollar of income gets assigned somewhere until you have zero left unaccounted for.

The free version requires you to enter transactions manually, which is fine if you’re just starting out. The premium version adds bank syncing, custom reports, and a “margin finder” that identifies breathing room in your budget.

It relaunched in early 2026 with daily lessons and live group coaching added to the premium plan, which is a nice touch for people who need guidance alongside the tool.

Best for: People focused on paying off debt who respond well to structure and coaching.

5. Monarch Money – Best for a Complete Financial Picture

If your money problems are less about daily overspending and more about never knowing where you actually stand financially, Monarch Money might be the answer.

It connects all your accounts – checking, savings, investments, loans – in one dashboard. You can see your net worth, track spending, set goals, and collaborate with a partner. It’s polished and gives you the kind of big-picture visibility that helps you make smarter long-term decisions.

It’s a paid subscription, but it’s one of the most well-rounded personal finance apps available right now.

Best for: People who want a full financial picture, not just a spending tracker.

Which One Should You Actually Download?

Here’s the honest answer:

- If you want to completely change how you handle money – YNAB

- If you just need to stop overspending day-to-day – PocketGuard

- If you want something free and simple to start – Goodbudget

- If you’re drowning in debt – EveryDollar

- If you want the full financial picture – Monarch Money

The best budgeting app isn’t the one with the most features. It’s the one you’ll actually open tomorrow morning. Start with whichever one feels the least intimidating and build from there.

Frequently Asked Questions

What is the easiest budgeting app for beginners? Goodbudget and PocketGuard are both great starting points. Goodbudget walks you through the envelope method step by step, while PocketGuard just shows you a safe-to-spend number without any setup.

Is YNAB worth the money if I’m broke? Yes, actually. YNAB offers a 34-day free trial, and most users report saving more than the subscription cost within their first month. If you’re living paycheck to paycheck, the structure it provides can be genuinely life-changing.

Can budgeting apps help me get out of debt? Apps like YNAB and EveryDollar both have debt payoff planning features built in. They won’t pay your debt for you, but they help you find extra money to throw at it each month.

Are budgeting apps safe to connect to my bank? Yes, as long as you use a reputable app. All the apps on this list use bank-level encryption and don’t store your full login credentials.